Planning your finances for the entire year is one of the most effective ways to stay organized, curb impulse spending, and hit your long-term money goals. This annual budget planner printable helps you manage your yearly income, monthly fixed costs, variable expenses, savings targets, debt paydowns, and big-picture financial goals all in one centralized place.

Whether you’re creating your very first comprehensive budget or refining your existing household financial habits, this printable worksheet gives you a clear, high-level overview of your finances for the entire 12 months. Designed in standard US Letter (8.5 × 11″) size, it is perfectly formatted for budget binders, home planners, and physical finance tracking systems.

Download Your Free Annual Budget Planner Printable

Note: Click the link below to download your high-resolution, print-ready PDF file instantly. No email signup required.

Download Your Free Annual Budget Planner Printable

Organize your finances for the entire year with this free Annual Budget Planner Printable PDF. Plan your yearly income, budget every expense category, track savings, monitor debt payments, and achieve your financial goals with this easy-to-use printable worksheet.

{kind=link}

What Is an Annual Budget Planner?

An annual budget planner printable is a high-level personal finance framework designed to map out your projected income and cash outflows over a full calendar year. Unlike a standard monthly budget sheet, which only looks at immediate bills, a yearly budget planner printable zooms out to capture macro trends, seasonal spending spikes, and long-term wealth accumulation goals.

Why Yearly Budget Planning Shifts Your Financial Trajectory

Most financial mistakes don’t happen because people can’t pay their regular monthly rent or electric bills. They happen because people get blindsided by irregular, non-recurring expenses—like semi-annual car insurance premiums, holiday shopping budgets, annual property taxes, or seasonal home maintenance costs.

When you use a yearly finance planner, you transform these surprising, high-stress expenses into predictable, pre-planned line items on an annual budget worksheet. You are no longer playing financial defense; you are proactively telling your money exactly where to go months before it ever hits your bank account.

The True Psychological Benefits of Long-Term Financial Planning

Tracking your income, daily expenses, and dedicated savings goals across a full year reduces the chronic stress associated with money management. Instead of feeling isolated inside a difficult financial month, a printable yearly budget lets you see that a temporary spending spike in December or a vacation expense in July won’t ruin your long-term plans, provided the rest of your year is structurally balanced. It changes your focus from daily financial survival to intentional, generational wealth creation.

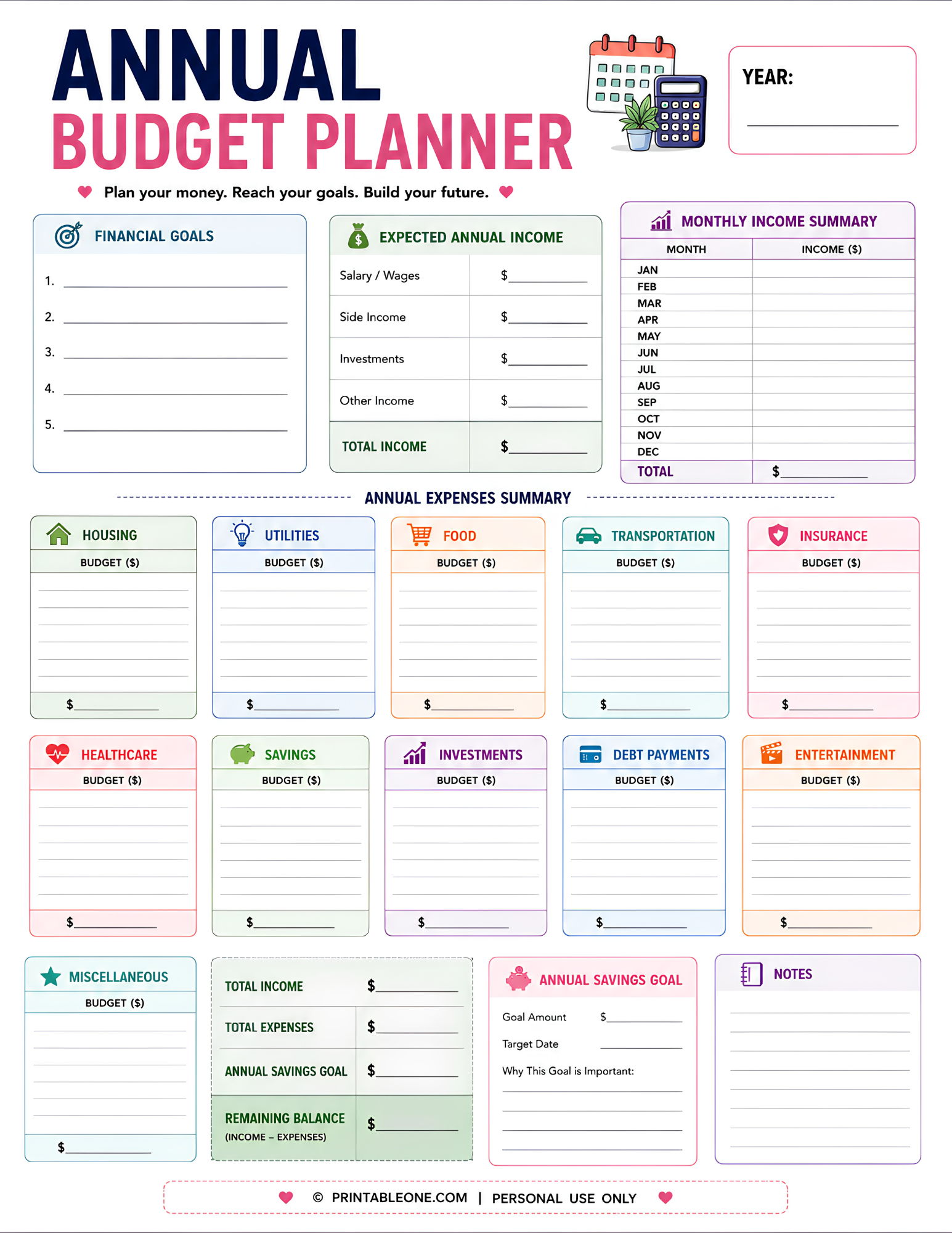

What’s Included in This Printable PDF?

This annual financial planner strips away the complex, glitchy formulas of digital macro spreadsheets, providing you with a clean, beautifully organized, and highly functional layout to manage your money with absolute confidence.

- Year & Goal Setting Section: A prominent anchor at the top of the page to log the current calendar year alongside your top-tier financial goals.

- Expected Annual Income Section: Dedicated calculation lines to tally up every projected source of revenue over the next 12 months.

- Comprehensive Expense Categories: Structured columns divided into core areas of life, including Housing, Utilities, Food, Transportation, Insurance, and Healthcare.

- Savings & Investment Trackers: Designated sections to map out your long-term emergency funds, retirement contributions, and personal brokerage deposits.

- Debt Payment Log: A high-visibility zone to plan out your principal reduction strategies for credit cards, auto financing, and student loans.

- Total Summary Block: A clean, bottom-of-the-page calculation grid to compare your aggregate annual income against your total planned outlays.

- Notes & Monthly Adjustments Section: A broad canvas at the base of the page for tracking variable market changes, lifestyle adjustments, or irregular windfall cash allocations.

How to Use This Annual Budget Planner

Filling out your budget planner printable PDF doesn’t require an accounting degree. Follow this clear, logical step-by-step walkthrough to map out your upcoming year accurately.

Step 1: Write Down the Calendar Year

Fill out the year section at the top of the worksheet. If you are starting mid-year, that is perfectly fine—simply label the sheet for the rolling 12-month period ahead.

Step 2: Set Tangible Financial Goals

State exactly what milestones you intend to cross over the next 12 months. Make these goals as specific and measurable as possible.

- Example: “Build a $10,000 fully-funded emergency fund.”

- Example: “Pay down $7,500 of high-interest credit card debt.”

- Example: “Maximize my personal Roth IRA contributions.”

Step 3: Estimate Your Total Yearly Income

Calculate your baseline net income (take-home pay after taxes and workplace deductions) from all available sources for the upcoming year using a yearly income planner.

Income Elements to Include:

• Primary corporate salary or hourly wages

• Secondary side hustles or freelance contracts

• Reliable business revenue or distributions

• Investment dividends or rental property cash flow

• Expected tax refunds or annual bonusesStep 4: Map Out Your Annual Expenses

Go through the core categories on your annual money planner and allocate funds for each bucket. For variable categories like groceries or gas, multiply your typical monthly average by 12. For non-recurring costs, note the exact month they occur.

Step 5: Tally the Total Numbers

Add up your entire income column to find your Gross Planned Income. Next, add up your absolute expenses, savings allocations, and debt paydowns to establish your Total Annual Outflows.

Step 6: Review the Remaining Balance

Subtract your total planned outflows from your gross planned income.

Your goal is to achieve a zero-based budget, meaning every single dollar earned is given a specific job (even if that job is going directly into a savings or investment bucket). If your remaining balance is negative, go back through your variable categories and prune unnecessary overhead until the sheet balances perfectly.

Step 7: Maintain an Active Monthly Tracking Review

Keep your personal finance planner inside an active household binder. At the close of every month, check your real-world progress against your yearly projections to make sure you aren’t drifting off course.

Annual vs. Monthly Budget Planning

To build long-term financial stability, you need to understand how these two distinct budgeting systems complement each other on a day-to-day basis.

| Features & Focus | Annual Budget Planning | Monthly Budget Planning |

| Strategic Scope | Long-term macro planning across 12 full months. | Short-term micro planning across 30 distinct days. |

| Primary Objective | Tracks grand yearly goals, net worth changes, and seasonal bills. | Tracks immediate daily spending, weekly grocery runs, and regular utilities. |

| Overview Capacity | Provides a comprehensive financial overview of your wealth trajectory. | Offers easier, highly detailed daily management of cash on hand. |

| Risk Mitigation | Prepares your bank account for major future or irregular expenses. | Controls current spending habits to ensure you don’t overdraw accounts. |

| Ideal Tool | Managed via a structural annual expense planner baseline sheet. | Executed via a detailed printable budget worksheet updated weekly. |

Deep Dive: Master Budget Categories

To prevent tracking confusion, categorize your planned household cash flow according to these industry-standard definitions on your yearly expense tracker:

Fixed Living Overhead

- Housing: Mortgage principal and interest payments, monthly rent payments, annual property taxes, home insurance premiums, and HOA dues.

- Utilities: Grid electricity, natural gas, municipal water/trash services, high-speed internet, mobile phone plans, and home security subscriptions.

- Insurance: Personal health insurance premiums, dental/vision coverage, term life insurance policies, long-term disability plans, and umbrella protection.

Variable Operational Expenses

- Food: Core weekly family groceries, household paper products, school lunches, and occasional dining out or food delivery orders.

- Transportation: Auto loan payments, fuel costs, regular oil changes and tire rotations, mass transit passes, parking fees, and annual vehicle registration.

- Healthcare: Medical co-pays, prescription medication refills, routine dental checkups, and general out-of-pocket health wellness expenses.

Wealth Building & Future Planning

- Yearly Savings Planner: Emergency fund cash reserves, specific sinking funds (holiday shopping, weddings, home repairs), and down payment accruals.

- Investment Planner: Individual brokerage accounts, index fund contributions, automated robo-advisor deposits, and real estate investment trusts (REITs).

- Debt Payments: Accelerated principal payments on credit card balances, personal signature loans, student loan balances, and home equity lines of credit.

8 Common Budgeting Mistakes That Destroy Financial Plans

Even the most well-intentioned individuals run into roadblocks when organizing a yearly budget template. Keeping an eye out for these classic pitfalls keeps your long-term money strategy intact.

- Omitting Irregular or “Sinking Fund” Bills: Forgetting about annual software renewals, pet vet checkups, car registration fees, or quarterly pest control treatments will instantly derail a monthly plan. Map these out across your full calendar year ahead of time.

- Setting Completely Unrealistic Spending Limits: Restricting your variable spending too aggressively—like cutting your grocery budget by 50% overnight—is a recipe for burnout. Keep your limits challenging but entirely grounded in historical reality.

- Failing to Track Small, Recurring Purchases: A $6 daily coffee run or an unmonitored streaming subscription doesn’t look like much in isolation, but over a full year, that single habit turns into a $2,000+ line item.

- Neglecting the Construction of an Emergency Fund: If you don’t build a dedicated buffer for unexpected car breakdowns or medical events, any emergency will force you to borrow money, instantly destroying your carefully planned budget lines.

- Forgetting to Factor in Special Event Seasons: Birthdays, summer vacations, weddings, and holiday gifting seasons happen at the exact same time every single year. Do not treat them like unexpected financial emergencies.

- Abandoning the Tracker After an Overspending Event: Budgeting is not about achieving absolute perfection; it is about maintaining situational awareness. If you overspend in January, don’t throw away the worksheet. Adjust your numbers for February and keep moving forward.

- Failing to Update the Budget When Real Income Shifts: If you experience a salary cut, a job change, or a sudden boost in income, you must recalculate your finance printable to match your actual cash flow reality immediately.

- Leaving One Partner Completely Out of the Planning Loop: For couples, a budget cannot be a unilateral decision. Both partners need to sit down together over the planner to ensure mutual buy-in and shared accountability for the goals written at the top.

Professional Budgeting Tips to Build Accelerated Wealth

- Implement a Paying-Yourself-First System: Instead of budgeting to see what money is left over to save at the end of the month, decide on your savings goals first. Route that cash directly into investments the day you get paid, then live comfortably on whatever remains.

- Utilize the Cash Envelope Method for Problem Categories: If you consistently overspend on variable items like clothing, entertainment, or dining out, use physical cash envelopes for those specific buckets. When the physical cash is gone for the month, your spending stops instantly.

- Regularly Prune and Audit Subscription Services: Twice a year, do a deep dive into your credit card statements. Cancel any app, streaming service, or gym membership you haven’t actively used in the past 30 days.

- Build Milestone Incentives Into Your Long-Term Plan: Staying disciplined over 12 full months is hard work. Celebrate your progress by building minor, affordable rewards into your plan whenever you hit a major milestone, like wiping out an individual credit card balance.

Who Should Use an Annual Budget Planner Printable?

This comprehensive worksheet is designed to be highly accessible and universally beneficial, fitting neatly into any lifestyle or financial structure.

- Busy Families & Households: A foundational anchor for managing multi-person expenses, keeping track of child activities, utility shifts, and major shared financial goals.

- College Students & Grads: An excellent educational framework to learn the mechanics of cash management, entry-level career salary allocations, and debt prevention.

- Freelancers, Gig Workers, & Solopreneurs: An absolute necessity for individuals with highly volatile monthly income, allowing you to establish a stable annual average so you don’t run out of money during slow seasons.

- Dedicated Budget Binder Lovers: Pristinely formatted to slip inside standard home command center binders alongside your physical calendars, meal planners, and chore logs.

Frequently Asked Questions

Is this annual budget planner completely free to download?

Yes. This downloadable PDF file is 100% free to print, copy, and distribute for personal financial tracking use as many times as you need throughout the year.

What are the exact dimensions of the printable sheet?

The layout is optimized specifically for standard US Letter dimensions (8.5 × 11 inches). It prints perfectly on all home office printers and fits cleanly into standard three-ring organizational binders.

Can I laminate my printed worksheet?

Absolutely. Lamination is highly recommended if you want to create a reusable dashboard. By using a standard dry-erase or wet-erase marker, you can update your rolling projections and monthly numbers on a single sheet without needing to reprint it constantly.

Should I update my annual tracker every single week?

No, weekly updates are usually overkill for a macro annual tracker. We recommend setting aside 20 minutes at the end of every month to review your numbers, track your structural progress, and log your actual spending data.

Can this document be used effectively by complete beginners?

Yes. The layout completely avoids confusing financial jargon or overly dense grid lines. If you know your estimated income and your basic monthly bills, the visual structure guides you through the entire calculation naturally.

Does this planner work well with other home organization trackers?

Yes. This layout is designed to serve as the macro foundation for your finances, working in harmony with specialized micro sheets like weekly spending trackers, debt snowball logs, and specific cash envelope systems.

Explore More Free Personal Finance Printables

To build out a truly comprehensive, custom-tailored financial management binder, pair your new annual sheet with our collection of high-functioning, matching printables:

- Monthly Budget Planner Printable: Dial in the exact day-to-day granular details of your income and variable cash outlays every 30 days.

- Paycheck Budget Planner Printable: Ideal for bi-weekly or semi-monthly earners who prefer to allocate their money the exact moment their paycheck hits their account.

- Expense Tracker Printable: A detailed, line-item ledger to record your daily physical and digital purchases to eliminate budget leaks completely.

- Net Worth Tracker Printable: Track your total assets against your outstanding liabilities to measure your real, long-term wealth growth month-over-month.

- Debt Snowball Tracker Printable: A highly motivating, visual milestone map to help you track your progress as you systematically crush your outstanding loans.

Final Thoughts

An organized, well-calibrated budget is the irreplaceable foundation of all long-term financial success. This annual budget planner printable gives you the clarity needed to take control of your income, contain runaway variable costs, grow your personal investments, and keep your focus locked onto your ultimate wealth goals all year long.

Download your free worksheet today, sit down with your numbers, and step into your financial future with complete clarity and confidence.